Leading Construction Index Produces Stability

Article Date: May 25, 2023

A Buoy of Optimism Amidst Uncertainty

The economic outlook detailed in daily headlines can be a maelstrom of mixed messages. Yet, in midst of the swirl, the construction industry appears to be a buoy of cautious optimism.

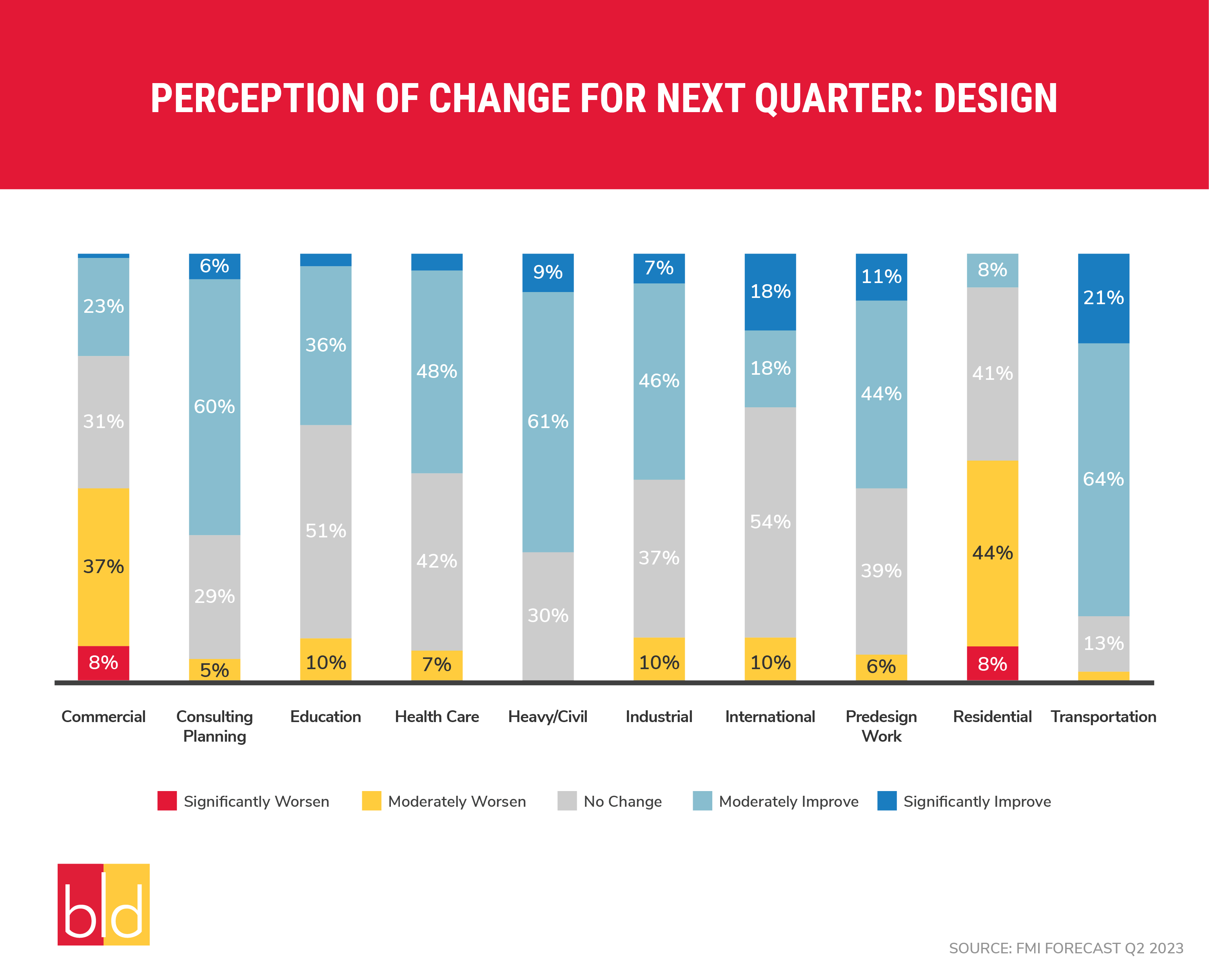

That is the leading takeaway from the first two quarter reports from the Construction Industry Round Table (CIRT) Index, a quarterly survey of 115-120 CEOs from the leading architectural, engineering, and construction firms doing business in the United States. The first quarter index, published by FMI, a leading consulting firm in the built environment, notched a positive view on the overall economy for the first time in five quarters. While overall sentiment dipped slightly in the second quarter, the Design Index increased again in Q2 – indicating that “more optimism about projects that haven’t reached the construction phase.”

That continues a positive run for the Design Index, an indicator of future projects now in planning, which jumped nearly 10 points in the first quarter.

More specifically, survey respondents were less bullish on the overall U.S. economy, “local economies where CIRT members operate, the overall nonresidential sector, and members’ construction businesses.”

What does this mean for building products brands as the calendar turns to spring selling season … and the summer months?

Let’s dig in.

Opportunity Awaits … in Certain Sectors

Optimism springs eternal, especially in the public works, transportation, industrial, and manufacturing sectors, according to the report.

Part of the opportunity is the recent passage of the Infrastructure Investment and Jobs Act, Inflation Reduction Act, CHIPs, and Science Act. More than half of respondents (55%) in the first quarter believed the federal legislation and resulting funding will impact business in 2023, with the greatest impact in hiring plans and market segment expansion.

Also, in the Q1 report, nearly all members (88%) expected some revenue impact, and 57% anticipated moderate impact on revenue. In fact, most members changed 2023 business strategy with the policy changes in mind.

“Transportation and heavy civil are the two areas projected to experience both short-term and long-term gains in design opportunities,” according to the FMI report. “In the construction space, manufacturing, public works, and transportation are seeing expanding opportunities over the short and long term.”

In the first quarter, a sense of cooling inflation and more favorable interest rates eased financial conditions and provided price stability, FMI reported. That adjusted in the second quarter with the impacts of recent bank failures with “nearly all respondents anticipating tightened lending standards for commercial real estate and construction, with the largest impacts in private commercial, private institutional and on projects of more than $100 million.”

In Q1, nearly 90% of CIRT members had at least 12 months of work planned; nearly two-thirds (65%) reported backlogs that are stronger going into 2023 than last year. Nearly half (47%) of respondents had more than 19 months of backlog, with 41% in the 12-18-month range.

Coping with Choppy Waters

While positive sentiment remains, the outlook is not all Ted Lasso-like in its enthusiasm. CIRT members expressed concern about the supply and retention of labor, with roughly half of them reporting higher hiring goals than last year, FMI reported in Q1.

Additionally in the second quarter report, more than a third of respondents (36%) experienced subcontractor defaults within the past two years with default frequency and severity increasing over the past year.

“Recent subcontractor defaults were most often attributed to supply chain and material prices escalations (60%), subcontractors taking on too much work (56%), and/or a lack of workers (52%),” the report said.

The last point continues a trend of labor supply concerns from the Q1 survey, which goes beyond skilled workers and includes a limited supply of field supervision (31%) and a limited supply of professional and management staff (31%).

What You Need to Know Before You Go

- In Q1, the CIRT Index notched a positive view on the overall economy with an uptick of 2.3 points, with stabilization in Q2.

- The most optimism is in the public works, transportation, industrial, and manufacturing sectors.

- Fifty-five percent believed recently passed federal legislation and resulting funding will impact business in 2023, with the greatest impact in hiring plans and market segment expansion.

- In Q1, the Design index jumped nearly 10 points over last quarter and increased again in Q2.

- Transportation and heavy civil project to experience short-term and long-term gains in design opportunities.

- Nearly 90% of CIRT members had at least 12 months of work planned.

- Labor supply and retention remains a concern.

- Material and equipment costs are an ongoing concern.

BLD Marketing is a results-based, digitally-focused, full-service strategic marketing firm exclusively serving the commercial and residential building materials category.